You built your crypto stack for a reason: long-term upside. But what happens when you need liquidity right now?

A lot of investors assume their only option is to sell. But selling triggers tax, reduces your exposure, and can leave you regretting the exit if the market rebounds. Borrowing gives you another path: unlock cash without giving up your position.

This guide breaks down, in plain language:

What happens when you sell your crypto

What happens when you borrow against it

When each option makes the most sense

How to borrow safely, transparently, and with minimal risk

Let’s dive in.

What happens when you sell crypto

Across both Canada and the United States, regulators treat crypto as property, not currency. That means selling, swapping, or spending crypto creates a taxable event.

Instead of selling your BTC or ETH, you can post it as collateral and borrow fiat (or stablecoin) against it. Increasingly, long-term holders use this to stay invested while accessing cash when they need it.

Is borrowing a taxable event?

In most jurisdictions, no.

A loan backed by crypto is not considered a sale, so you generally don’t trigger capital gains when the loan originates.

However:

If your collateral is liquidated, that may count as a disposal.

If you repay the loan in appreciated crypto, that may also trigger tax.

Some jurisdictions may treat things like wrapping (BTC → cbBTC), transfers, or interest differently. Always confirm with a tax professional.

Why borrowing can make sense

Stay invested: You keep exposure to future upside.

Defer tax: No realization event at origination.

Unlock cash: Use funds for real estate, business investment, or market opportunities.

Optionality: If markets run, you’re still in the game.

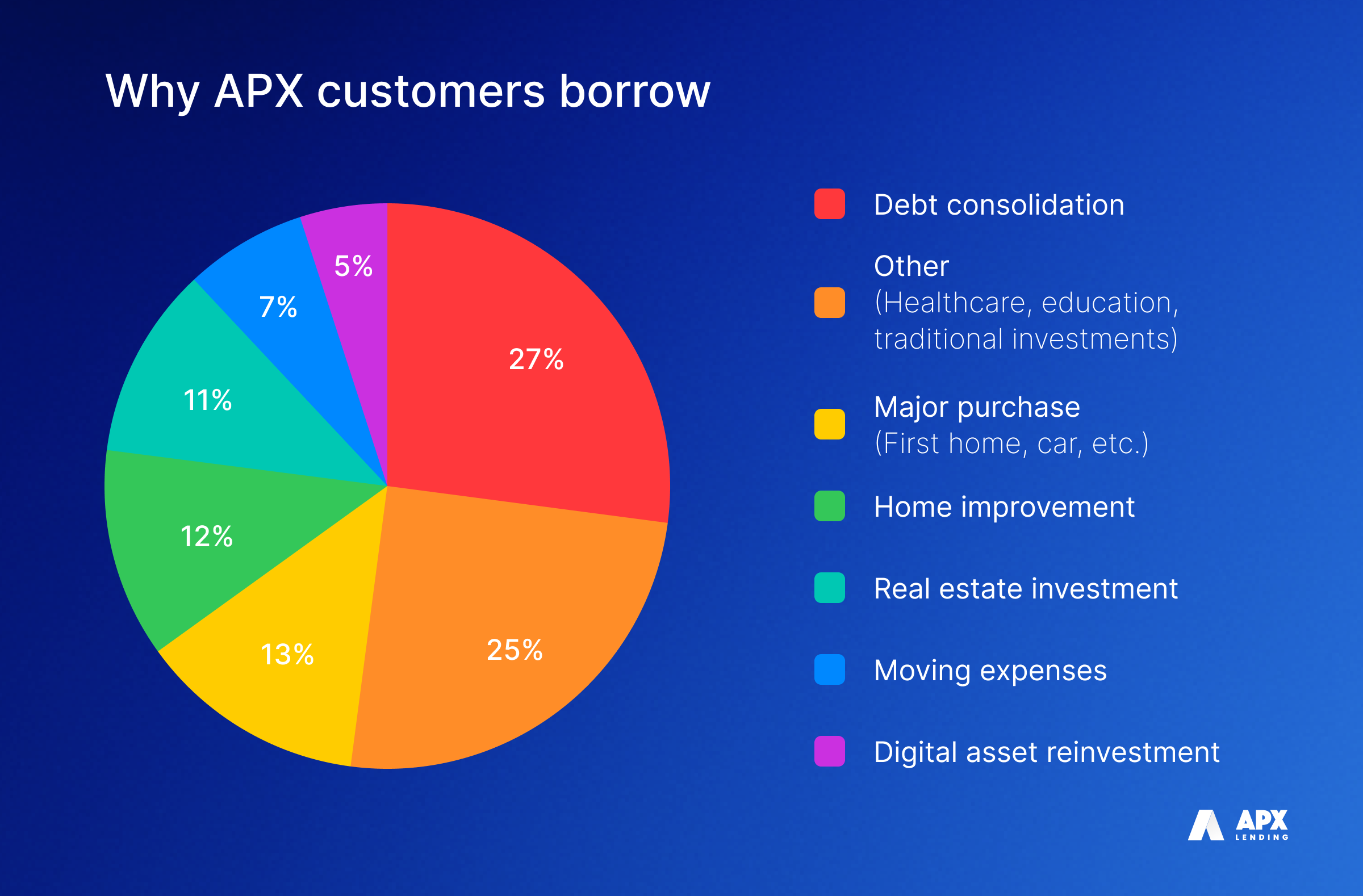

Many APX customers borrow for:

Down payments

Business expansion

Taxes or operational liquidity

Portfolio rebalancing without selling core holdings

Source: priopriatry data

Potential risks

Liquidation risk: If BTC or ETH drops and your LTV rises, your collateral may need a top-up. If liquidation risk is a real concern, check out our primer on crypto-loan liquidation.

Interest costs: Make sure borrowing costs are lower than the value you expect to preserve by not selling. For a convenient look at what the biggest lenders are charging, check out our platform-by-platform comparison guide.

Documentation: You’ll need clear records for tax purposes.

Repayment method: Repaying in crypto may trigger taxable disposal.

Borrow vs. sell: side-by-side comparison

Feature

Sell Crypto

Borrow Against Crypto

Tax event today

Yes — sale triggers capital gains

Usually no tax at origination

Ownership

You exit your position

You keep full market exposure

Liquidity timing

Instant upon sale

Fast, depending on lender

Market upside

None — you’re out

Fully retained

Risk of liquidation

None

Yes — tied to crypto price

Best for

Reducing exposure or exiting crypto

Staying invested while accessing cash

When borrowing makes the most sense

Borrowing is especially compelling when:

You believe your BTC or ETH will continue to appreciate

You need liquidity now but don’t want to exit your position

You’re using funds for high-ROI activities (business, real estate, reinvestment)

If your goal is to unlock cash today without giving up your crypto’s future upside, borrowing against your holdings can be a smart strategy, especially when done through a regulated, transparent lender.

If you’re ready to de-risk or exit positions, selling may be the better choice.

Whatever you choose, custody, compliance, and clarity matter. APX Lending is designed to give Canadian and U.S. investors a safe, regulated way to borrow against their crypto without taking on platform risk.

Generally no — unless your collateral is later liquidated or you repay the loan with appreciated crypto.

Is borrowing against crypto taxable in the U.S.?

Loan origination is usually not taxable, but liquidation or crypto-based repayment may be.

Do I still own my Bitcoin when I use it as collateral?

You keep exposure to price moves. The lender simply holds it under the agreed custody terms.

Is interest deductible?

It depends on your jurisdiction, whether the loan is for investment or business use, and your personal tax profile. Consult your tax advisor.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

Borrow vs. sell: The tax-smart way to access your Bitcoin

Borrow vs. sell: The tax-smart way to access your Bitcoin

Explainer

December 17, 2025

5min read

You built your crypto stack for a reason: long-term upside. But what happens when you need liquidity right now?

A lot of investors assume their only option is to sell. But selling triggers tax, reduces your exposure, and can leave you regretting the exit if the market rebounds. Borrowing gives you another path: unlock cash without giving up your position.

This guide breaks down, in plain language:

What happens when you sell your crypto

What happens when you borrow against it

When each option makes the most sense

How to borrow safely, transparently, and with minimal risk

Let’s dive in.

What happens when you sell crypto

Across both Canada and the United States, regulators treat crypto as property, not currency. That means selling, swapping, or spending crypto creates a taxable event.

Instead of selling your BTC or ETH, you can post it as collateral and borrow fiat (or stablecoin) against it. Increasingly, long-term holders use this to stay invested while accessing cash when they need it.

Is borrowing a taxable event?

In most jurisdictions, no.

A loan backed by crypto is not considered a sale, so you generally don’t trigger capital gains when the loan originates.

However:

If your collateral is liquidated, that may count as a disposal.

If you repay the loan in appreciated crypto, that may also trigger tax.

Some jurisdictions may treat things like wrapping (BTC → cbBTC), transfers, or interest differently. Always confirm with a tax professional.

Why borrowing can make sense

Stay invested: You keep exposure to future upside.

Defer tax: No realization event at origination.

Unlock cash: Use funds for real estate, business investment, or market opportunities.

Optionality: If markets run, you’re still in the game.

Many APX customers borrow for:

Down payments

Business expansion

Taxes or operational liquidity

Portfolio rebalancing without selling core holdings

Source: priopriatry data

Potential risks

Liquidation risk: If BTC or ETH drops and your LTV rises, your collateral may need a top-up. If liquidation risk is a real concern, check out our primer on crypto-loan liquidation.

Interest costs: Make sure borrowing costs are lower than the value you expect to preserve by not selling. For a convenient look at what the biggest lenders are charging, check out our platform-by-platform comparison guide.

Documentation: You’ll need clear records for tax purposes.

Repayment method: Repaying in crypto may trigger taxable disposal.

Borrow vs. sell: side-by-side comparison

Feature

Sell Crypto

Borrow Against Crypto

Tax event today

Yes — sale triggers capital gains

Usually no tax at origination

Ownership

You exit your position

You keep full market exposure

Liquidity timing

Instant upon sale

Fast, depending on lender

Market upside

None — you’re out

Fully retained

Risk of liquidation

None

Yes — tied to crypto price

Best for

Reducing exposure or exiting crypto

Staying invested while accessing cash

When borrowing makes the most sense

Borrowing is especially compelling when:

You believe your BTC or ETH will continue to appreciate

You need liquidity now but don’t want to exit your position

You’re using funds for high-ROI activities (business, real estate, reinvestment)

If your goal is to unlock cash today without giving up your crypto’s future upside, borrowing against your holdings can be a smart strategy, especially when done through a regulated, transparent lender.

If you’re ready to de-risk or exit positions, selling may be the better choice.

Whatever you choose, custody, compliance, and clarity matter. APX Lending is designed to give Canadian and U.S. investors a safe, regulated way to borrow against their crypto without taking on platform risk.

Generally no — unless your collateral is later liquidated or you repay the loan with appreciated crypto.

Is borrowing against crypto taxable in the U.S.?

Loan origination is usually not taxable, but liquidation or crypto-based repayment may be.

Do I still own my Bitcoin when I use it as collateral?

You keep exposure to price moves. The lender simply holds it under the agreed custody terms.

Is interest deductible?

It depends on your jurisdiction, whether the loan is for investment or business use, and your personal tax profile. Consult your tax advisor.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

We use cookies to enhance your browsing experience, analyze site traffic, and personalize content. By clicking 'Accept,' you consent to the use of cookies as described in our Privacy Policy.

%201%20(3).png)

.png)

.webp)