How crypto loan interest rates work: fixed rates, LTV, and payment plans

Crypto-backed loans have gone mainstream, and for good reason. Whether you hold Bitcoin or Ethereum, they’re an efficient way to access liquidity without selling your assets. But one question we conistently here from borrowers is:

How do crypto loan interest rates actually work?

Thankfully, the answer is simple.

Unlike DeFi lending markets, where rates fluctuate constantly, CeFi lenders use fixed interest rates, predictable terms, and clear loan-to-value (LTV) thresholds. That stability makes borrowing against your crypto far more straightforward than many expect.

This guide breaks down how fixed crypto loan rates are set, how LTV impacts your cost, and how to choose between interest-only and amortized payment plans.

What a crypto loan interest rate really is

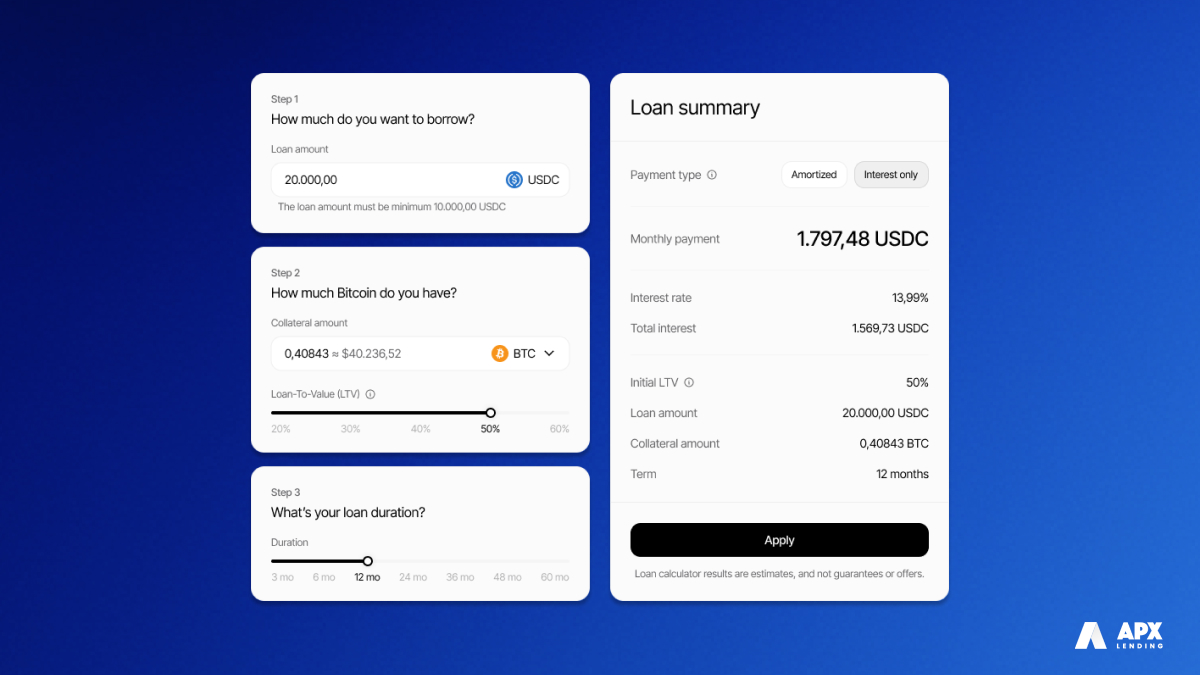

A crypto loan interest rate is the cost of borrowing cash using your digital assets as collateral. In CeFi, interest rates are fixed for the full term, typically 6 to 36 months (3 to 60 for us), so your monthly payment stays the same.

Most reputable lenders fall somewhere in the 8% – 16% APR range, which can depend on several key factors, like: the lender cost of capital, LTV, collateral type, and custody model.

Every lender uses its own risk model, but fixed rates generally reflect five core factors.

Cost of capital

Behind every crypto loan rate is a lender’s cost of capital, the cost of sourcing the money they lend out. If that cost rises, rates rise. If it falls, rates fall. Regulated CeFi lenders often use a mix of treasury reserves, credit facilities, and institutional partners to supply capital. Lenders who rely on expensive deposits or unsecured credit lines tend to have higher, more volatile rates.

APX uses a conservative capital structure with segregated collateral custody, which allows us to maintain stable, transparent pricing without relying on risky rehypothecation practices.

Loan-to-value (LTV)

For some lenders, LTV ratio can influence rates. In the interest of keeping things simple and offering as much flexibility as possible to our lenders, APX doesn't do this.

Lower LTV = lower risk = lower interest rate.

LTV tiers:

LTV range

Risk level

Expected rate

20–30%

Low

Lowest rates

35–50%

Medium

Mid-range rates

60%+

High

Highest rates

Collateral type: Bitcoin vs. Ethereum

Because Bitcoin is less volatile and more liquid than Ethereum, BTC-backed loans often receive slightly lower rates.

ETH’s higher volatility introduces more collateral risk, which introduces a slightly higher cost of capital for lenders.

Origination fees: what they are and how they affect your total cost

Along with interest rates, most lenders charge an origination fee. This is a one-time cost added at the beginning of your loan. Origination fees typically range from 1% to 4% of the loan amount, depending on the lender’s operating model and risk framework.

You can look at an origination fee as the cost of provisioning your loan, including:

Onboarding and compliance (KYC/AML)

Operational and custody expenses

Underwriting and risk assessment

Capital sourcing and processing

Regulatory obligations for registered lenders

Because crypto loans are often larger than typical consumer loans, and because lenders bear collateral-management responsibilities, origination fees are common across the industry.

At APX, we do not charge origination fees. Everything is baked in to your final rate in the interest of keeping things simple and transparent. In other words, what you see when you confirm your loan agreement is what you get.

How origination fees impact borrowing:

They’re a one-time cost, not a recurring payment

They do not change your interest rate

They slightly increase your total cost of borrowing

Regulatory and compliance requirements

Regulated CeFi lenders like APX typically maintain:

Risk reserves

Strict KYC/AML controls

Transparent loan terms

Standardized liquidation procedures

This framework results in more predictable rates compared to offshore or unregulated lenders, where prices fluctuate to offset systemic and operational risk. If you want to learn more about the standards we hold ourselves to, as the only crypto lender to-date that is authorized by the CSA, you can read our decision here.

→ Variable rates → Rates change based on liquidity pools → Designed for traders, not long-term borrowers

Borrowers looking for stability and long-term planning almost always prefer fixed-rate CeFi loans. They're safe, secure, and predictable.

Interest-only vs. amortized crypto loans

Your repayment structure significantly impacts your monthly budget and total lifetime cost. APX, like many other bitcoin-backed lenders, offers two payment options: interest-only and amortized.

Interest-only payments mean you pay only the interest during your term. Your principal stays intact until the final balloon payment which you must settle upon your loan’s maturation date.

Best for:

Long-term BTC or ETH holders

Borrowers who expect asset appreciation

Anyone needing maximum cash flow flexibility

Businesses, founders, and miners

Advantages

Lowest possible monthly payment

More liquidity retained

Maintains long-term crypto exposure

Useful for short-term liquidity (taxes, real estate bridging, business runway)

Trade-offs

Principal is due at the end, which means a large payment

Most borrowers know their answer within minutes of reviewing their calculator output.

Why borrowers choose fixed-rate crypto loans

Borrowing against Bitcoin or Ethereum makes sense when:

You want liquidity without triggering capital gains tax

You believe BTC/ETH will appreciate over time

You prefer predictable, stable monthly payments

You want to avoid selling during volatility

You need access to cash for investments or expenses

APX’s regulated framework, fixed-rate structure, and cold-storage custody make borrowing far safer than the early days of crypto lending.

FAQs

Are crypto loan rates fixed?

Most regulated CeFi lenders, including APX, use fixed interest rates. Your rate stays the same for the full term, making monthly payments predictable.

Is an interest-only crypto loan better?

Interest-only loans offer the lowest monthly payment and the most liquidity. They’re ideal if you want to keep your crypto exposure while accessing cash.

What affects my crypto loan rate?

Rates depend on LTV, collateral type (Bitcoin or Ethereum), custody standards, and the lender’s regulatory framework.

Does borrowing against crypto trigger taxes?

No. Borrowing does not trigger a taxable event in Canada or the U.S. because you're not selling your crypto. Always consult a tax professional for personal guidance.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

How crypto loan interest rates work: fixed rates, LTV, and payment plans

How crypto loan interest rates work: fixed rates, LTV, and payment plans

Explainer

December 12, 2025

5min read

How crypto loan interest rates work: fixed rates, LTV, and payment plans

Crypto-backed loans have gone mainstream, and for good reason. Whether you hold Bitcoin or Ethereum, they’re an efficient way to access liquidity without selling your assets. But one question we conistently here from borrowers is:

How do crypto loan interest rates actually work?

Thankfully, the answer is simple.

Unlike DeFi lending markets, where rates fluctuate constantly, CeFi lenders use fixed interest rates, predictable terms, and clear loan-to-value (LTV) thresholds. That stability makes borrowing against your crypto far more straightforward than many expect.

This guide breaks down how fixed crypto loan rates are set, how LTV impacts your cost, and how to choose between interest-only and amortized payment plans.

What a crypto loan interest rate really is

A crypto loan interest rate is the cost of borrowing cash using your digital assets as collateral. In CeFi, interest rates are fixed for the full term, typically 6 to 36 months (3 to 60 for us), so your monthly payment stays the same.

Most reputable lenders fall somewhere in the 8% – 16% APR range, which can depend on several key factors, like: the lender cost of capital, LTV, collateral type, and custody model.

Every lender uses its own risk model, but fixed rates generally reflect five core factors.

Cost of capital

Behind every crypto loan rate is a lender’s cost of capital, the cost of sourcing the money they lend out. If that cost rises, rates rise. If it falls, rates fall. Regulated CeFi lenders often use a mix of treasury reserves, credit facilities, and institutional partners to supply capital. Lenders who rely on expensive deposits or unsecured credit lines tend to have higher, more volatile rates.

APX uses a conservative capital structure with segregated collateral custody, which allows us to maintain stable, transparent pricing without relying on risky rehypothecation practices.

Loan-to-value (LTV)

For some lenders, LTV ratio can influence rates. In the interest of keeping things simple and offering as much flexibility as possible to our lenders, APX doesn't do this.

Lower LTV = lower risk = lower interest rate.

LTV tiers:

LTV range

Risk level

Expected rate

20–30%

Low

Lowest rates

35–50%

Medium

Mid-range rates

60%+

High

Highest rates

Collateral type: Bitcoin vs. Ethereum

Because Bitcoin is less volatile and more liquid than Ethereum, BTC-backed loans often receive slightly lower rates.

ETH’s higher volatility introduces more collateral risk, which introduces a slightly higher cost of capital for lenders.

Origination fees: what they are and how they affect your total cost

Along with interest rates, most lenders charge an origination fee. This is a one-time cost added at the beginning of your loan. Origination fees typically range from 1% to 4% of the loan amount, depending on the lender’s operating model and risk framework.

You can look at an origination fee as the cost of provisioning your loan, including:

Onboarding and compliance (KYC/AML)

Operational and custody expenses

Underwriting and risk assessment

Capital sourcing and processing

Regulatory obligations for registered lenders

Because crypto loans are often larger than typical consumer loans, and because lenders bear collateral-management responsibilities, origination fees are common across the industry.

At APX, we do not charge origination fees. Everything is baked in to your final rate in the interest of keeping things simple and transparent. In other words, what you see when you confirm your loan agreement is what you get.

How origination fees impact borrowing:

They’re a one-time cost, not a recurring payment

They do not change your interest rate

They slightly increase your total cost of borrowing

Regulatory and compliance requirements

Regulated CeFi lenders like APX typically maintain:

Risk reserves

Strict KYC/AML controls

Transparent loan terms

Standardized liquidation procedures

This framework results in more predictable rates compared to offshore or unregulated lenders, where prices fluctuate to offset systemic and operational risk. If you want to learn more about the standards we hold ourselves to, as the only crypto lender to-date that is authorized by the CSA, you can read our decision here.

→ Variable rates → Rates change based on liquidity pools → Designed for traders, not long-term borrowers

Borrowers looking for stability and long-term planning almost always prefer fixed-rate CeFi loans. They're safe, secure, and predictable.

Interest-only vs. amortized crypto loans

Your repayment structure significantly impacts your monthly budget and total lifetime cost. APX, like many other bitcoin-backed lenders, offers two payment options: interest-only and amortized.

Interest-only payments mean you pay only the interest during your term. Your principal stays intact until the final balloon payment which you must settle upon your loan’s maturation date.

Best for:

Long-term BTC or ETH holders

Borrowers who expect asset appreciation

Anyone needing maximum cash flow flexibility

Businesses, founders, and miners

Advantages

Lowest possible monthly payment

More liquidity retained

Maintains long-term crypto exposure

Useful for short-term liquidity (taxes, real estate bridging, business runway)

Trade-offs

Principal is due at the end, which means a large payment

Most borrowers know their answer within minutes of reviewing their calculator output.

Why borrowers choose fixed-rate crypto loans

Borrowing against Bitcoin or Ethereum makes sense when:

You want liquidity without triggering capital gains tax

You believe BTC/ETH will appreciate over time

You prefer predictable, stable monthly payments

You want to avoid selling during volatility

You need access to cash for investments or expenses

APX’s regulated framework, fixed-rate structure, and cold-storage custody make borrowing far safer than the early days of crypto lending.

FAQs

Are crypto loan rates fixed?

Most regulated CeFi lenders, including APX, use fixed interest rates. Your rate stays the same for the full term, making monthly payments predictable.

Is an interest-only crypto loan better?

Interest-only loans offer the lowest monthly payment and the most liquidity. They’re ideal if you want to keep your crypto exposure while accessing cash.

What affects my crypto loan rate?

Rates depend on LTV, collateral type (Bitcoin or Ethereum), custody standards, and the lender’s regulatory framework.

Does borrowing against crypto trigger taxes?

No. Borrowing does not trigger a taxable event in Canada or the U.S. because you're not selling your crypto. Always consult a tax professional for personal guidance.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

We use cookies to enhance your browsing experience, analyze site traffic, and personalize content. By clicking 'Accept,' you consent to the use of cookies as described in our Privacy Policy.

%201%20(3).png)

.png)

.webp)