Trust

APX Lending has 0 exposure to the Coldcard exploit

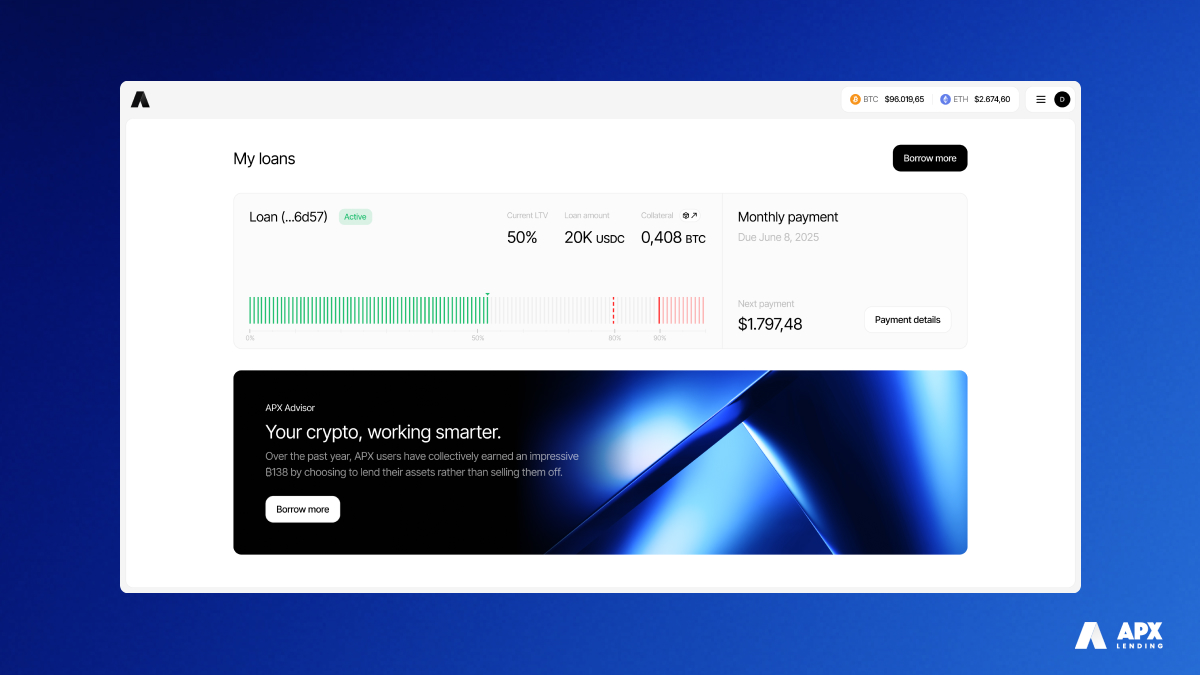

Our borrowers also have 24/7 visibility into their collateral, both on-chain and through the APX platform. No guess work, no questions, full and absolute transparency.

August 3, 2026

Read more

.jpg)

We launched APX Lending with the ambition of building something durable: a crypto-backed lending platform that could function in real market conditions, under real regulatory scrutiny, and still serve borrowers when volatility inevitably returned.

Over the past year, that idea was tested.

Crypto markets, and Bitcoin in particular, went through one of the most volatile years on record, marked by sharp swings that put real pressure on crypto lending models.

Regulatory pressure increased worldwide, with the U.S.’s GENIUS Act and Canada’s drafted Stablecoins Act, among other key initiatives in the EU, Hong Kong and the UAE.

The last few years have shown which crypto lending models can endure prolonged volatility and which break down once the going gets rough. Through it all, APX continued operating as designed, without mass liquidations, without emergency policy changes, and without compromising borrower trust.

As we mark the end of the year, this feels like the right moment to look back at what we built, what changed across the crypto landscape, and why we believe regulated crypto-backed lending is here to stay.

Crypto-backed lending has existed since the late teens. What’s been rarer is a model that balances borrower flexibility with institutional-grade custody, conservative risk management, and regulatory alignment across jurisdictions.

From day one, APX was built around those constraints. That meant slower decisions in some areas, more scrutiny in others, and a willingness to say no when a faster path would have introduced unnecessary risk.

Those choices matter most when the market turns.

On April 1, 2025, APX reached a milestone that fundamentally changed our position in the marketplace.

APX Lending became the first crypto-backed lender globally to receive approval from the Canadian Securities Administrators, following a decision led by the Ontario Securities Commission.

This wasn’t a symbolic gesture. It involved several years of work with the regulators in Canada to develop a framework of what a compliant crypto-backed lending model could operate in practice: how collateral is held, how risks are disclosed, how loans are monitored, and how borrowers are protected. The result is a lender operating under oversight comparable to traditional financial institutions, with consumer protections not consistently present across the crypto lending market.

Beyond this, APX continued operating as a registered entity with FINTRAC (M23366277) and FinCEN (31000248116781) and received SOC 2 compliance to formalize our internal security and operational controls.

Altogether, these steps reflect something we’ve believed from the start: crypto-backed lending can and should operate within existing financial and regulatory frameworks.

If Bitcoin is the world’s greatest asset, it deserves the greatest protection as it enters the credit industry at scale and 2026 was the inflection point where Bitcoin stopped being viewed purely as a speculative asset by the legacy financial system and started being treated as usable collateral inside real credit systems. Its journey mirrored how other asset classes evolved - first traded, then custody/standards, then credit.

This year included a sharp Bitcoin drawdown, with prices in November 2025 dropping as much as 30%. Naturally, this put considerable pressure on crypto lending platforms across the industry.

For many borrowers elsewhere, that period meant forced liquidations, sudden margin calls, or frozen access to funds. In some cases, it meant discovering too late that risk policies weren’t built for sustained volatility.

APX’s experience was different.

Because of conservative loan-to-value ratios (47% average across our users), continuous monitoring, and clear borrower communication, APX did not experience widespread liquidations during the downturn. Loans remained intact. Borrowers retained control. Systems behaved the way they were designed to behave.

In the interest of full transparency, here are the numbers:

That outcome wasn’t accidental. It was the result of building for downside scenarios rather than optimizing solely for peak demand.

In crypto lending, surviving a bear market isn’t a bonus, it’s the baseline. This year confirmed that APX’s approach doesn’t just help us weather difficult markets. It helps us thrive inside them.

While regulatory milestones defined much of the year externally, internally we focused on making the borrowing experience more flexible and fairer for our borrowers.

In September, we launched our “Borrow more” feature, allowing existing borrowers to access additional liquidity from their posted collateral without closing or refinancing their original loan. Minimums remain $10,000 CAD in Canada and $25,000 USDC in the U.S., but the feature significantly improves flexibility for long-term holders and allows our offering to behave more like a line of credit.

In October, we updated our interest rates. Previously set at a flat 13.99%, the new structure is more borrower-friendly and better reflects actual risk and market conditions. The principle was straightforward: if we can responsibly offer better terms, we absolutely should.

While these are our posted rates at time of writing, we are constantly negotiating better terms with our credit facilities in an effort to pass along best-in-market terms to our customers.

In November, we launched our referral program, generously rewarding customers who introduce their friends to APX. Word of mouth has always mattered in crypto, and our users continue to be some of our strongest advocates.

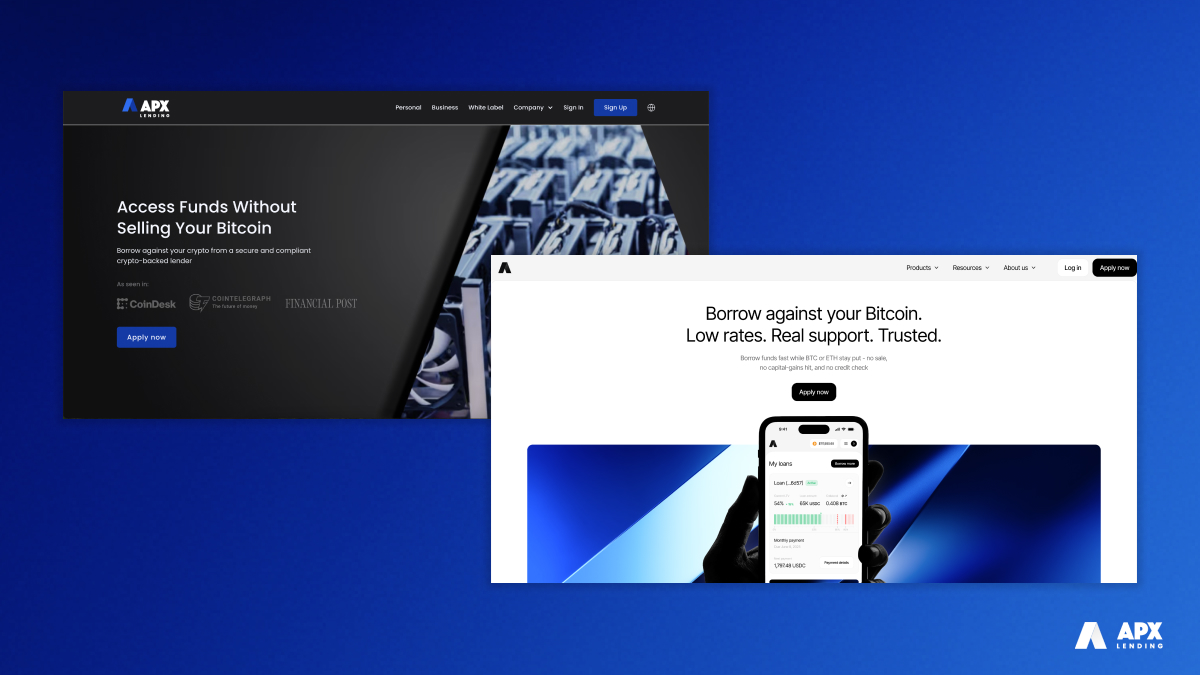

Earlier in the fall, we also rolled out a refreshed look across the APX app and website. The update focused on clarity and speed, while keeping the same human support borrowers expect.

It should come as no surprise to learn that these updates have significantly improved our ability to deploy loans fast. This year, we achieved a new record, from user creation to loan deployed in just over two hours. That's ten to twenty times faster than other lenders, proving that regulatory, safety and compliance, don't have to come at the cost of an excellent user experience and speed.

At the same time, USDC-denominated loans went live in Ontario, with ambitions to offer them Canada-wide, expanding stablecoin options within a regulated framework.

This year also marked meaningful progress in partnerships and distribution.

We have expanded our white-label lending programs across North America and the EU, allowing platforms to offer crypto-backed loans under their own brands.

The EU expansion is especially important. Operating in one of the most regulated financial environments globally, and doing so seamlessly, reinforced our belief that compliance doesn’t slow good products down. It makes them scalable and, most importantly, safe.

The broader crypto regulatory environment also shifted this year, particularly in Canada and the U.S.

In Canada, securities regulators have continued tightening expectations for crypto platforms, particularly around client asset custody, segregation, and risk disclosures, as evidenced by CSA Staff Notice 21-332 and CSA Staff Notice 21-333, which expand investor protection requirements for crypto asset trading platforms. APX’s CSA authorization reflects that regulatory direction and the higher operational standards now expected of compliant crypto lenders.

The CSA also issued a reminder that any crypto-backed lenders operating within its jurisdiction must prepare for potential regulatory requirements.

Finally, Canada has drafted its own Stablecoins Act, an encouraging sign of the country’s adoption of digital currencies.

In the U.S., regulatory and legislative progress in 2025 provided clearer guardrails for digital assets, even as the overall framework remains distributed across agencies. The GENIUS Act established the first comprehensive federal framework for payment stablecoins, including 1:1 reserve requirements, monthly audit disclosures, and consumer protections for stablecoin issuers.

At the same time, the continued growth and record assets under management in spot Bitcoin ETFs have signaled growing institutional participation in regulated investment products. Regulators such as the CFTC have introduced initiatives like pilot programs and tokenized collateral guidance, reflecting a shift toward incorporating digital assets into existing regulated markets.

Across both markets, the trend is clear. Crypto financial services are being pulled into the mainstream regulatory perimeter. For lending platforms, that shift favors models built for transparency and resilience.

Throughout the year, APX remained active in the crypto community, speaking and participating at events including Consensus, Bitcoin 2025, Blockchain Futurist Conference, and Tokenize! Global.

The conversations were consistent. Crypto-backed loans aren’t going away, but they are maturing alongside the wider industry.

If this past year was about proving resilience, the next phase is about responsible growth.

That means expanding internationally with care, continuing to improve borrower terms, and working with regulators rather than around them. It means building lending products that function just as well in downturns as they do in bull markets and help usher the next phase of the adoption curve for crypto and Bitcoin specifically – entry into the credit industry.

This past year proved that our approach is working.

We’re proud of what we’ve built so far, and we’re focused on what comes next.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

We launched APX Lending with the ambition of building something durable: a crypto-backed lending platform that could function in real market conditions, under real regulatory scrutiny, and still serve borrowers when volatility inevitably returned.

Over the past year, that idea was tested.

Crypto markets, and Bitcoin in particular, went through one of the most volatile years on record, marked by sharp swings that put real pressure on crypto lending models.

Regulatory pressure increased worldwide, with the U.S.’s GENIUS Act and Canada’s drafted Stablecoins Act, among other key initiatives in the EU, Hong Kong and the UAE.

The last few years have shown which crypto lending models can endure prolonged volatility and which break down once the going gets rough. Through it all, APX continued operating as designed, without mass liquidations, without emergency policy changes, and without compromising borrower trust.

As we mark the end of the year, this feels like the right moment to look back at what we built, what changed across the crypto landscape, and why we believe regulated crypto-backed lending is here to stay.

Crypto-backed lending has existed since the late teens. What’s been rarer is a model that balances borrower flexibility with institutional-grade custody, conservative risk management, and regulatory alignment across jurisdictions.

From day one, APX was built around those constraints. That meant slower decisions in some areas, more scrutiny in others, and a willingness to say no when a faster path would have introduced unnecessary risk.

Those choices matter most when the market turns.

On April 1, 2025, APX reached a milestone that fundamentally changed our position in the marketplace.

APX Lending became the first crypto-backed lender globally to receive approval from the Canadian Securities Administrators, following a decision led by the Ontario Securities Commission.

This wasn’t a symbolic gesture. It involved several years of work with the regulators in Canada to develop a framework of what a compliant crypto-backed lending model could operate in practice: how collateral is held, how risks are disclosed, how loans are monitored, and how borrowers are protected. The result is a lender operating under oversight comparable to traditional financial institutions, with consumer protections not consistently present across the crypto lending market.

Beyond this, APX continued operating as a registered entity with FINTRAC (M23366277) and FinCEN (31000248116781) and received SOC 2 compliance to formalize our internal security and operational controls.

Altogether, these steps reflect something we’ve believed from the start: crypto-backed lending can and should operate within existing financial and regulatory frameworks.

If Bitcoin is the world’s greatest asset, it deserves the greatest protection as it enters the credit industry at scale and 2026 was the inflection point where Bitcoin stopped being viewed purely as a speculative asset by the legacy financial system and started being treated as usable collateral inside real credit systems. Its journey mirrored how other asset classes evolved - first traded, then custody/standards, then credit.

This year included a sharp Bitcoin drawdown, with prices in November 2025 dropping as much as 30%. Naturally, this put considerable pressure on crypto lending platforms across the industry.

For many borrowers elsewhere, that period meant forced liquidations, sudden margin calls, or frozen access to funds. In some cases, it meant discovering too late that risk policies weren’t built for sustained volatility.

APX’s experience was different.

Because of conservative loan-to-value ratios (47% average across our users), continuous monitoring, and clear borrower communication, APX did not experience widespread liquidations during the downturn. Loans remained intact. Borrowers retained control. Systems behaved the way they were designed to behave.

In the interest of full transparency, here are the numbers:

That outcome wasn’t accidental. It was the result of building for downside scenarios rather than optimizing solely for peak demand.

In crypto lending, surviving a bear market isn’t a bonus, it’s the baseline. This year confirmed that APX’s approach doesn’t just help us weather difficult markets. It helps us thrive inside them.

While regulatory milestones defined much of the year externally, internally we focused on making the borrowing experience more flexible and fairer for our borrowers.

In September, we launched our “Borrow more” feature, allowing existing borrowers to access additional liquidity from their posted collateral without closing or refinancing their original loan. Minimums remain $10,000 CAD in Canada and $25,000 USDC in the U.S., but the feature significantly improves flexibility for long-term holders and allows our offering to behave more like a line of credit.

In October, we updated our interest rates. Previously set at a flat 13.99%, the new structure is more borrower-friendly and better reflects actual risk and market conditions. The principle was straightforward: if we can responsibly offer better terms, we absolutely should.

While these are our posted rates at time of writing, we are constantly negotiating better terms with our credit facilities in an effort to pass along best-in-market terms to our customers.

In November, we launched our referral program, generously rewarding customers who introduce their friends to APX. Word of mouth has always mattered in crypto, and our users continue to be some of our strongest advocates.

Earlier in the fall, we also rolled out a refreshed look across the APX app and website. The update focused on clarity and speed, while keeping the same human support borrowers expect.

It should come as no surprise to learn that these updates have significantly improved our ability to deploy loans fast. This year, we achieved a new record, from user creation to loan deployed in just over two hours. That's ten to twenty times faster than other lenders, proving that regulatory, safety and compliance, don't have to come at the cost of an excellent user experience and speed.

At the same time, USDC-denominated loans went live in Ontario, with ambitions to offer them Canada-wide, expanding stablecoin options within a regulated framework.

This year also marked meaningful progress in partnerships and distribution.

We have expanded our white-label lending programs across North America and the EU, allowing platforms to offer crypto-backed loans under their own brands.

The EU expansion is especially important. Operating in one of the most regulated financial environments globally, and doing so seamlessly, reinforced our belief that compliance doesn’t slow good products down. It makes them scalable and, most importantly, safe.

The broader crypto regulatory environment also shifted this year, particularly in Canada and the U.S.

In Canada, securities regulators have continued tightening expectations for crypto platforms, particularly around client asset custody, segregation, and risk disclosures, as evidenced by CSA Staff Notice 21-332 and CSA Staff Notice 21-333, which expand investor protection requirements for crypto asset trading platforms. APX’s CSA authorization reflects that regulatory direction and the higher operational standards now expected of compliant crypto lenders.

The CSA also issued a reminder that any crypto-backed lenders operating within its jurisdiction must prepare for potential regulatory requirements.

Finally, Canada has drafted its own Stablecoins Act, an encouraging sign of the country’s adoption of digital currencies.

In the U.S., regulatory and legislative progress in 2025 provided clearer guardrails for digital assets, even as the overall framework remains distributed across agencies. The GENIUS Act established the first comprehensive federal framework for payment stablecoins, including 1:1 reserve requirements, monthly audit disclosures, and consumer protections for stablecoin issuers.

At the same time, the continued growth and record assets under management in spot Bitcoin ETFs have signaled growing institutional participation in regulated investment products. Regulators such as the CFTC have introduced initiatives like pilot programs and tokenized collateral guidance, reflecting a shift toward incorporating digital assets into existing regulated markets.

Across both markets, the trend is clear. Crypto financial services are being pulled into the mainstream regulatory perimeter. For lending platforms, that shift favors models built for transparency and resilience.

Throughout the year, APX remained active in the crypto community, speaking and participating at events including Consensus, Bitcoin 2025, Blockchain Futurist Conference, and Tokenize! Global.

The conversations were consistent. Crypto-backed loans aren’t going away, but they are maturing alongside the wider industry.

If this past year was about proving resilience, the next phase is about responsible growth.

That means expanding internationally with care, continuing to improve borrower terms, and working with regulators rather than around them. It means building lending products that function just as well in downturns as they do in bull markets and help usher the next phase of the adoption curve for crypto and Bitcoin specifically – entry into the credit industry.

This past year proved that our approach is working.

We’re proud of what we’ve built so far, and we’re focused on what comes next.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

%201%20(3).png)

.png)

.webp)