Most financial services haven’t figured out how to create more value out of this wealth. This is where crypto-backed lending comes in.

Bitcoin and Ethereum are increasingly held long term by retail, high-net-worth, and institutional clients. These assets may be custodied at exchanges, held with qualified custodians, or self-custodied entirely. Whatever the case, they exist in financial ecosystems that financial platforms already serve.

In other words, the business opportunity is real. And it’s already been quantified.

Offering crypto-backed lending allows exchanges, fintechs, and regulated financial institutions to:

Introduce a lending product without holding crypto on their own balance sheet

Monetize existing client relationships tied to digital asset holdings

Increase customer lifetime value and retention

Add a credit product without building lending infrastructure in-house

White-label crypto lending exists to make all the above simple and straightforward. It allows financial platforms to launch crypto-backed loans under their own brand, while relying on purpose-built infrastructure to handle custody, compliance, and risk.

Why crypto-native platforms led crypto-backed lending

Crypto-native platforms already have what lenders spend years trying to acquire:

Users who hold valuable collateral

Established trust and daily engagement

On-chain and off-chain data to support underwriting

What they often don’t have is the appetite to take on:

Regulatory risk

Custody complexity

Loan servicing and liquidation infrastructure

White-label crypto lending closes that gap. It allows platforms to offer crypto-backed loans under their own brand, while outsourcing the operational lift to regulated infrastructure.

For users, the value proposition is simple: access cash without selling Bitcoin or Ethereum and benefit from upside.

For platforms, it’s about turning passive balances into real value, for their customers and their underlying businesses.

The real cost of building crypto lending in-house

On paper, building a lending product sounds manageable. In reality, lending is one of the most operationally demanding products in financial services.

To do it properly, platforms must solve for:

Custody

Real-time LTV monitoring and margin logic

Liquidation workflows during volatility

AML, KYC, and transaction monitoring

Provisioning and servicing the entire loan lifecycle

Customer support

Regulatory reporting across regions

That’s before factoring in audits, security reviews, and incident response.

For most, this complexity pulls focus away from core roadmap priorities. It’s also why many early crypto lenders failed. Not due to lack of demand, but lack of controls.

White-label crypto lending platforms like APX Lending exist specifically to absorb this complexity, allowing partners to launch lending without rebuilding their stack or assuming unnecessary risk.

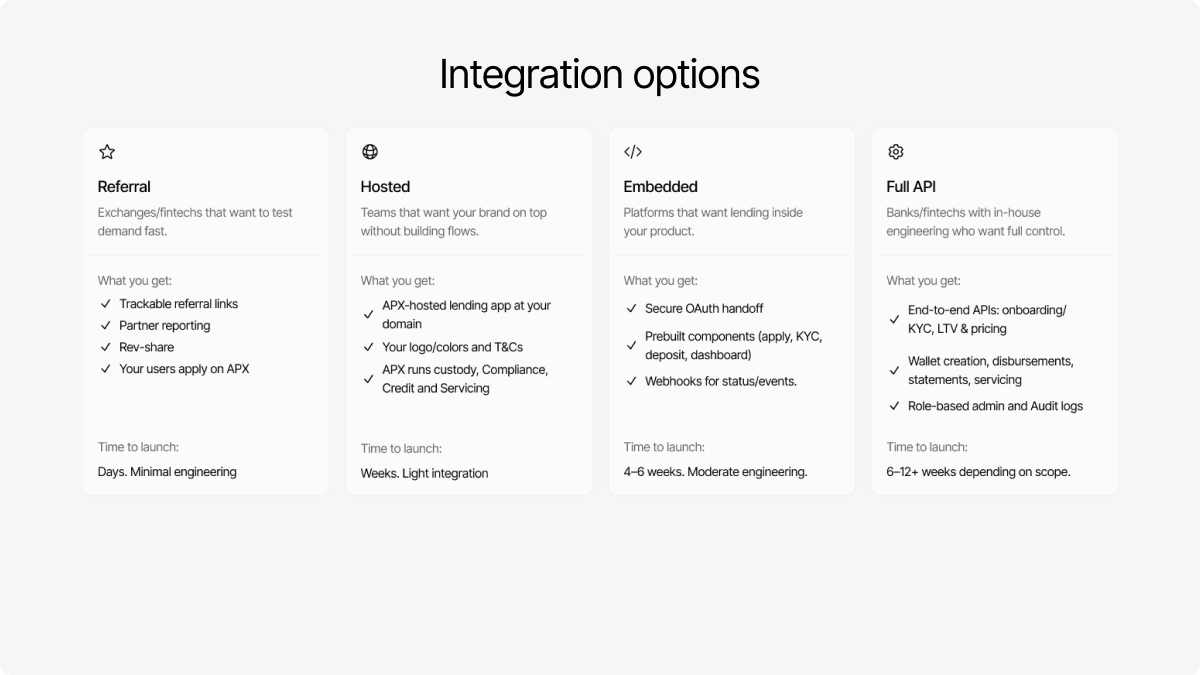

How white-label crypto lending works in practice

White-label lending isn’t a one-size-fits-all approach. Different platforms integrate at different depths depending on their technical maturity and product goals. Others, like APX Lending, provide total scalability, from lightweight referral programs to fully integrated platforms.

APX Lending integration options

API-first integrations

For platforms with engineering teams, lending can be embedded directly into existing apps via APIs. The loan experience feels native to users, while APX handles collateral management, underwriting, and servicing behind the scenes.

Hosted, branded lending flows

Platforms that want speed over customization can launch hosted lending flows branded to match their product. This is often the fastest path to market and a common starting point before deeper integration.

Embedded calculators and referral flows

For ecosystem partners, including advisors, accountants, and crypto service providers, lending can be offered via iframe calculators or referral links embedded directly on partner sites. This lets you unlock crypto lending without the burden of technical lift.

Why regulation is a feature, not a constraint

Crypto lending has matured. The market has seen what happens when leverage, custody, and credit operate without oversight.

As the Bank for International Settlements (BIS) has repeatedly noted, lending against volatile assets requires robust risk management and regulatory alignment. The same conclusion has been reinforced by post-mortems on failed crypto lenders.

For platforms operating in North America and Europe, regulation is no longer optional. It’s table stakes, and it’s precisely what enables long-term growth.

Combines crypto-native lending with institutional safeguards, allowing platforms to scale lending without absorbing full risk.

For platforms planning to operate long term, the choice is increasingly clear.

How traditional financial institutions are entering crypto-backed lending

While crypto exchanges are leading adoption, traditional financial institutions are beginning to follow.

Banks and fintechs are exploring crypto-backed lending as a way to offer digital asset exposure without holding crypto directly. White-label infrastructure allows them to partner with crypto-native platforms rather than compete with them.

For exchanges, this opens up:

Institutional partnerships

New distribution channels

Opportunities to expand into regulated financial ecosystems

Scaling across North America and Europe

North America remains the core market for regulated crypto lending, but Europe is emerging quickly. Germany, in particular, has taken a more structured approach to digital asset regulation, creating opportunities for compliant lending products.

APX Lending white-labels clients across North America and the E.U.

White-label infrastructure allows platforms to expand regionally without re-architecting their lending stack for each market—a meaningful advantage as crypto lending expands across markets.

Lending without losing control

White-label crypto lending allows platforms to add a capital-intensive product without becoming a capital-intensive business.

You control the brand, the user experience, and the customer relationship. APX operates behind the scenes, managing custody, customer support, compliance, and risk.

That separation is what makes white-label lending scalable.

Get in touch

If you’re exploring white-label crypto lending, whether through full API integration or lightweight embedded solutions, get in touch with APX Lending to discuss how it could work for your platform.

White-label crypto lending lets financial platforms offer crypto-backed loans under their own brand,

without building custody, compliance, underwriting, or servicing infrastructure in-house.

Who is white-label crypto lending for?

It’s built for crypto exchanges, wallets, fintechs, and regulated financial institutions that serve clients holding digital assets

and want to add lending without operating a full lending stack.

Do we need to custody crypto to offer lending?

No. Platforms don’t need to hold crypto on their own balance sheet. Depending on the integration model, loans can be offered against

client-held assets custodied at exchanges, qualified custodians, or in self-custody.

How do integration options work?

Partners can choose lightweight referral/iframe flows, hosted branded flows, or full API integrations. The right option depends on your

product goals, timeline, and engineering resources.

What does APX handle behind the scenes?

Custody and segregation, compliance programs, underwriting, collateral monitoring, servicing, and operational workflows—so your platform can

focus on distribution and the customer experience.

Is white-label crypto lending regulated?

Yes. Regulatory alignment is essential for institutional crypto lending. APX is built to support compliant crypto-backed lending in North America,

with controls designed for regulated partners.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

Most financial services haven’t figured out how to create more value out of this wealth. This is where crypto-backed lending comes in.

Bitcoin and Ethereum are increasingly held long term by retail, high-net-worth, and institutional clients. These assets may be custodied at exchanges, held with qualified custodians, or self-custodied entirely. Whatever the case, they exist in financial ecosystems that financial platforms already serve.

In other words, the business opportunity is real. And it’s already been quantified.

Offering crypto-backed lending allows exchanges, fintechs, and regulated financial institutions to:

Introduce a lending product without holding crypto on their own balance sheet

Monetize existing client relationships tied to digital asset holdings

Increase customer lifetime value and retention

Add a credit product without building lending infrastructure in-house

White-label crypto lending exists to make all the above simple and straightforward. It allows financial platforms to launch crypto-backed loans under their own brand, while relying on purpose-built infrastructure to handle custody, compliance, and risk.

Why crypto-native platforms led crypto-backed lending

Crypto-native platforms already have what lenders spend years trying to acquire:

Users who hold valuable collateral

Established trust and daily engagement

On-chain and off-chain data to support underwriting

What they often don’t have is the appetite to take on:

Regulatory risk

Custody complexity

Loan servicing and liquidation infrastructure

White-label crypto lending closes that gap. It allows platforms to offer crypto-backed loans under their own brand, while outsourcing the operational lift to regulated infrastructure.

For users, the value proposition is simple: access cash without selling Bitcoin or Ethereum and benefit from upside.

For platforms, it’s about turning passive balances into real value, for their customers and their underlying businesses.

The real cost of building crypto lending in-house

On paper, building a lending product sounds manageable. In reality, lending is one of the most operationally demanding products in financial services.

To do it properly, platforms must solve for:

Custody

Real-time LTV monitoring and margin logic

Liquidation workflows during volatility

AML, KYC, and transaction monitoring

Provisioning and servicing the entire loan lifecycle

Customer support

Regulatory reporting across regions

That’s before factoring in audits, security reviews, and incident response.

For most, this complexity pulls focus away from core roadmap priorities. It’s also why many early crypto lenders failed. Not due to lack of demand, but lack of controls.

White-label crypto lending platforms like APX Lending exist specifically to absorb this complexity, allowing partners to launch lending without rebuilding their stack or assuming unnecessary risk.

How white-label crypto lending works in practice

White-label lending isn’t a one-size-fits-all approach. Different platforms integrate at different depths depending on their technical maturity and product goals. Others, like APX Lending, provide total scalability, from lightweight referral programs to fully integrated platforms.

APX Lending integration options

API-first integrations

For platforms with engineering teams, lending can be embedded directly into existing apps via APIs. The loan experience feels native to users, while APX handles collateral management, underwriting, and servicing behind the scenes.

Hosted, branded lending flows

Platforms that want speed over customization can launch hosted lending flows branded to match their product. This is often the fastest path to market and a common starting point before deeper integration.

Embedded calculators and referral flows

For ecosystem partners, including advisors, accountants, and crypto service providers, lending can be offered via iframe calculators or referral links embedded directly on partner sites. This lets you unlock crypto lending without the burden of technical lift.

Why regulation is a feature, not a constraint

Crypto lending has matured. The market has seen what happens when leverage, custody, and credit operate without oversight.

As the Bank for International Settlements (BIS) has repeatedly noted, lending against volatile assets requires robust risk management and regulatory alignment. The same conclusion has been reinforced by post-mortems on failed crypto lenders.

For platforms operating in North America and Europe, regulation is no longer optional. It’s table stakes, and it’s precisely what enables long-term growth.

Combines crypto-native lending with institutional safeguards, allowing platforms to scale lending without absorbing full risk.

For platforms planning to operate long term, the choice is increasingly clear.

How traditional financial institutions are entering crypto-backed lending

While crypto exchanges are leading adoption, traditional financial institutions are beginning to follow.

Banks and fintechs are exploring crypto-backed lending as a way to offer digital asset exposure without holding crypto directly. White-label infrastructure allows them to partner with crypto-native platforms rather than compete with them.

For exchanges, this opens up:

Institutional partnerships

New distribution channels

Opportunities to expand into regulated financial ecosystems

Scaling across North America and Europe

North America remains the core market for regulated crypto lending, but Europe is emerging quickly. Germany, in particular, has taken a more structured approach to digital asset regulation, creating opportunities for compliant lending products.

APX Lending white-labels clients across North America and the E.U.

White-label infrastructure allows platforms to expand regionally without re-architecting their lending stack for each market—a meaningful advantage as crypto lending expands across markets.

Lending without losing control

White-label crypto lending allows platforms to add a capital-intensive product without becoming a capital-intensive business.

You control the brand, the user experience, and the customer relationship. APX operates behind the scenes, managing custody, customer support, compliance, and risk.

That separation is what makes white-label lending scalable.

Get in touch

If you’re exploring white-label crypto lending, whether through full API integration or lightweight embedded solutions, get in touch with APX Lending to discuss how it could work for your platform.

White-label crypto lending lets financial platforms offer crypto-backed loans under their own brand,

without building custody, compliance, underwriting, or servicing infrastructure in-house.

Who is white-label crypto lending for?

It’s built for crypto exchanges, wallets, fintechs, and regulated financial institutions that serve clients holding digital assets

and want to add lending without operating a full lending stack.

Do we need to custody crypto to offer lending?

No. Platforms don’t need to hold crypto on their own balance sheet. Depending on the integration model, loans can be offered against

client-held assets custodied at exchanges, qualified custodians, or in self-custody.

How do integration options work?

Partners can choose lightweight referral/iframe flows, hosted branded flows, or full API integrations. The right option depends on your

product goals, timeline, and engineering resources.

What does APX handle behind the scenes?

Custody and segregation, compliance programs, underwriting, collateral monitoring, servicing, and operational workflows—so your platform can

focus on distribution and the customer experience.

Is white-label crypto lending regulated?

Yes. Regulatory alignment is essential for institutional crypto lending. APX is built to support compliant crypto-backed lending in North America,

with controls designed for regulated partners.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

We use cookies to enhance your browsing experience, analyze site traffic, and personalize content. By clicking 'Accept,' you consent to the use of cookies as described in our Privacy Policy.

.jpg)

.png)

%201%20(3).png)

.png)

.webp)