Case Study

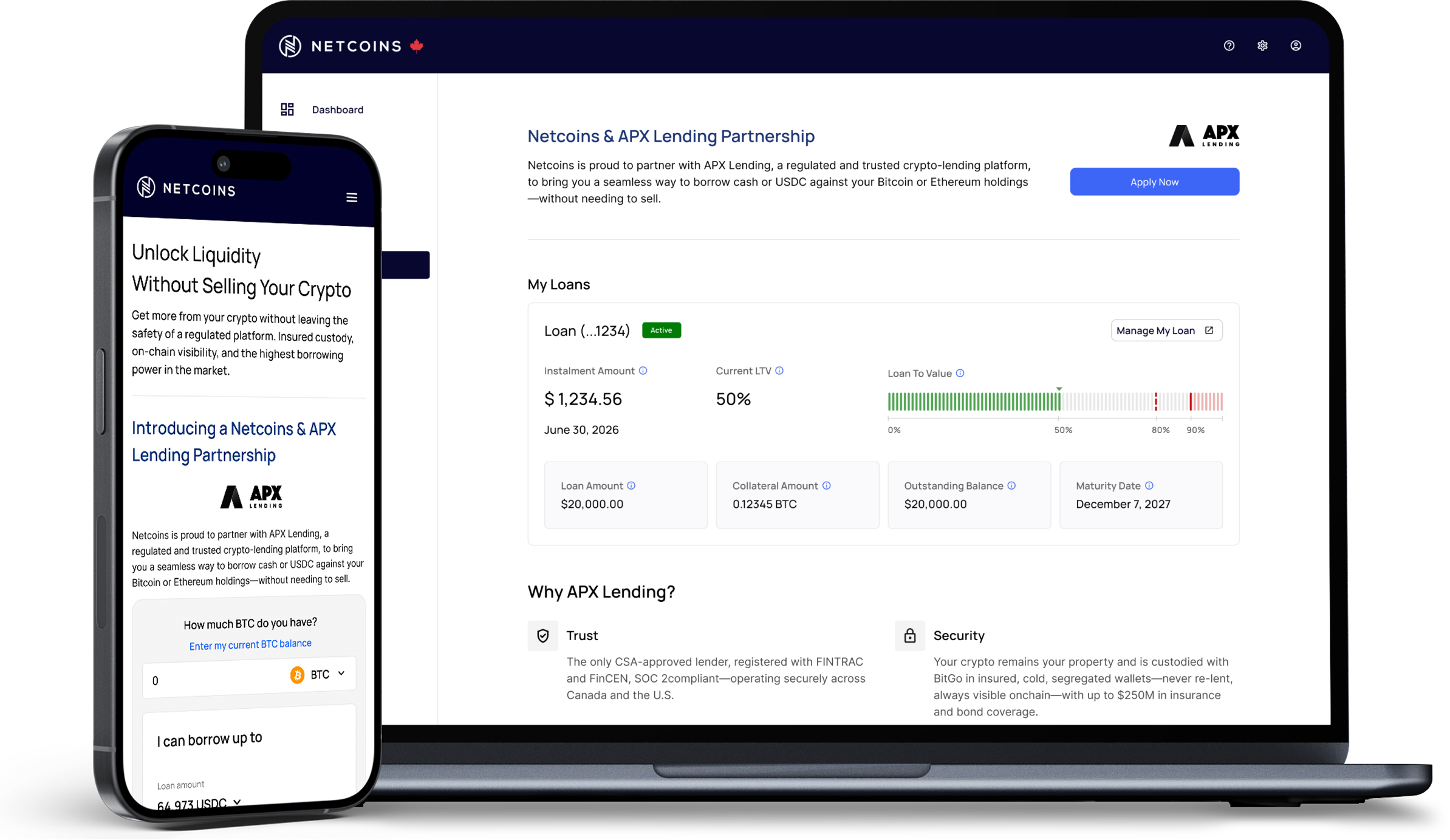

Netcoins and APX Lending: Canada's First Integrated Crypto-Backed Lending Experience

August 7, 2026

Read more

Imagine this: You own a meaningful amount of Bitcoin or Ethereum. You believe in its long-term upside, but you also have real-world cash needs: a down payment on property, an unexpected tax bill, business expansion, or simply wanting to retain exposure while unlocking liquidity.

Historically, you’d have to sell. But what if you could tap your crypto’s value like you tap your traditional investments with a line of credit instead?

This is what crypto credit is all about and why it represents the next frontier in digital-asset finance.

Loans are transactional. You borrow a fixed amount, repay on a fixed schedule, and exit the transaction once you’ve hit maturation.

Credit lines are different: they stay open, renew automatically, let you draw when you want, repay when you want and give you flexibility.

At APX Lending, we structure our offering like a crypto line of credit (with some differences):

Instead of “take a one-time loan,” you get “open a reusable line of credit powered by your crypto.”

That shift opens up a world of new possibilities.

Once upon a time, only office buildings, bullion or highly rated bonds served as collateral for credit lines.

Now, a few things have changed:

In other words, crypto isn’t just a speculative asset anymore. It’s becoming a genuine collateral class. That means you can unlock value while staying invested.

The first wave of crypto lenders offered easy liquidity but lacked essential safeguards. Many failed because they rehypothecated collateral, mixed client assets, and operated without oversight. When markets dropped, clients paid the price.

Global regulators took note:

These frameworks created a foundation for regulated crypto credit. Safer for borrowers, auditable for institutions, and transparent by design.

Here’s how the credit-line style product looks in practice:

This product gives you the flexibility of credit with the security of a regulated fintech lender.

What this means for retail and HNW borrowers

For HNW individuals, miners, family offices and business owners:

Key terms to understand

Why “crypto credit” is a game-changer

By framing your borrowing capacity as a credit line, you shift your mindset from “I’m cash-poor, I’m forced to sell” to “I hold optionality, I can borrow when it makes sense”. That difference matters for:

It also places APX Lending not just as a lender, but as a partner in your wealth strategy.

Getting started: your roadmap

Crypto credit is more than a niche product—it’s the next chapter of digital-asset finance. It gives you liquidity without surrendering upside, optionality instead of forced sales, and a trusted partner rather than an offshore risk.

At APX Lending, we’ve built a framework that blends credit-line flexibility with regulated custody, transparent thresholds, and institutional-grade stability. If you’re ready to think differently about how crypto supports your goals, we’re ready to walk alongside you.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

Imagine this: You own a meaningful amount of Bitcoin or Ethereum. You believe in its long-term upside, but you also have real-world cash needs: a down payment on property, an unexpected tax bill, business expansion, or simply wanting to retain exposure while unlocking liquidity.

Historically, you’d have to sell. But what if you could tap your crypto’s value like you tap your traditional investments with a line of credit instead?

This is what crypto credit is all about and why it represents the next frontier in digital-asset finance.

Loans are transactional. You borrow a fixed amount, repay on a fixed schedule, and exit the transaction once you’ve hit maturation.

Credit lines are different: they stay open, renew automatically, let you draw when you want, repay when you want and give you flexibility.

At APX Lending, we structure our offering like a crypto line of credit (with some differences):

Instead of “take a one-time loan,” you get “open a reusable line of credit powered by your crypto.”

That shift opens up a world of new possibilities.

Once upon a time, only office buildings, bullion or highly rated bonds served as collateral for credit lines.

Now, a few things have changed:

In other words, crypto isn’t just a speculative asset anymore. It’s becoming a genuine collateral class. That means you can unlock value while staying invested.

The first wave of crypto lenders offered easy liquidity but lacked essential safeguards. Many failed because they rehypothecated collateral, mixed client assets, and operated without oversight. When markets dropped, clients paid the price.

Global regulators took note:

These frameworks created a foundation for regulated crypto credit. Safer for borrowers, auditable for institutions, and transparent by design.

Here’s how the credit-line style product looks in practice:

This product gives you the flexibility of credit with the security of a regulated fintech lender.

What this means for retail and HNW borrowers

For HNW individuals, miners, family offices and business owners:

Key terms to understand

Why “crypto credit” is a game-changer

By framing your borrowing capacity as a credit line, you shift your mindset from “I’m cash-poor, I’m forced to sell” to “I hold optionality, I can borrow when it makes sense”. That difference matters for:

It also places APX Lending not just as a lender, but as a partner in your wealth strategy.

Getting started: your roadmap

Crypto credit is more than a niche product—it’s the next chapter of digital-asset finance. It gives you liquidity without surrendering upside, optionality instead of forced sales, and a trusted partner rather than an offshore risk.

At APX Lending, we’ve built a framework that blends credit-line flexibility with regulated custody, transparent thresholds, and institutional-grade stability. If you’re ready to think differently about how crypto supports your goals, we’re ready to walk alongside you.

APX Lending is a crypto-backed lender operating in the US, Canada, and globally. APX Lending does not offer financial or tax advice. We strongly encourage you to consult with a certified financial or tax professional for guidance on any related inquiries you may have.

%201%20(3).png)

.webp)